Why is Budgeting Important for Students?

University/College is a time of newfound freedom, but it also comes with significant financial responsibility. Creating a budget is essential for students because it helps them:

- Track income and expenses

- Avoid debt accumulation

- Achieve financial goals (e.g., saving for a trip, paying for textbooks)

- Reduce financial stress

- Develop good financial habits for the future

Understanding Your Income and Expenses

Identifying Income Sources

The first step in creating a budget is to understand where your money comes from. Common income sources for students include:

- Part-time jobs: Earnings from on-campus or off-campus employment.

- Allowances from parents/guardians: Regular financial support.

- Scholarships and grants: Financial aid that doesn't need to be repaid.

- Student loans: Borrowed money for education expenses (remember these need to be repaid!).

- Freelance work: Income from gigs like writing, tutoring, or web design.

- Investments: Returns from savings or investment accounts.

Tracking Your Expenses

Next, you need to know where your money is going. Expenses can be categorized as fixed or variable:

- Fixed expenses: These are relatively constant each month, such as rent, tuition, and loan payments.

- Variable expenses: These fluctuate, including groceries, entertainment, transportation, and dining out.

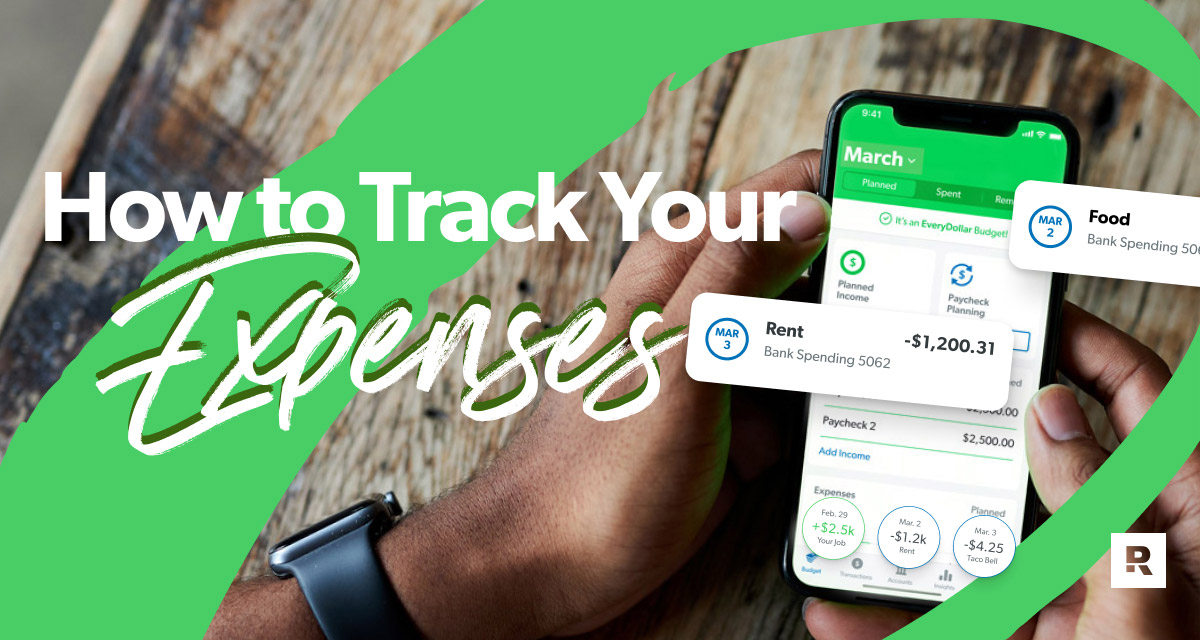

To effectively track your expenses, consider these methods:

- Use a budgeting app: Apps like Mint, YNAB (You Need a Budget), and PocketSmith can automate expense tracking.

- Keep a spreadsheet: Manually record your income and expenses in a tool like Google Sheets or Microsoft Excel.

- Review bank statements: Check your monthly statements to see where your money was spent.

- Save receipts: Collect receipts for a week or two to get a detailed snapshot of your spending habits.

Creating Your Student Budget

Budgeting Methods

Several budgeting methods can help you allocate your funds effectively:

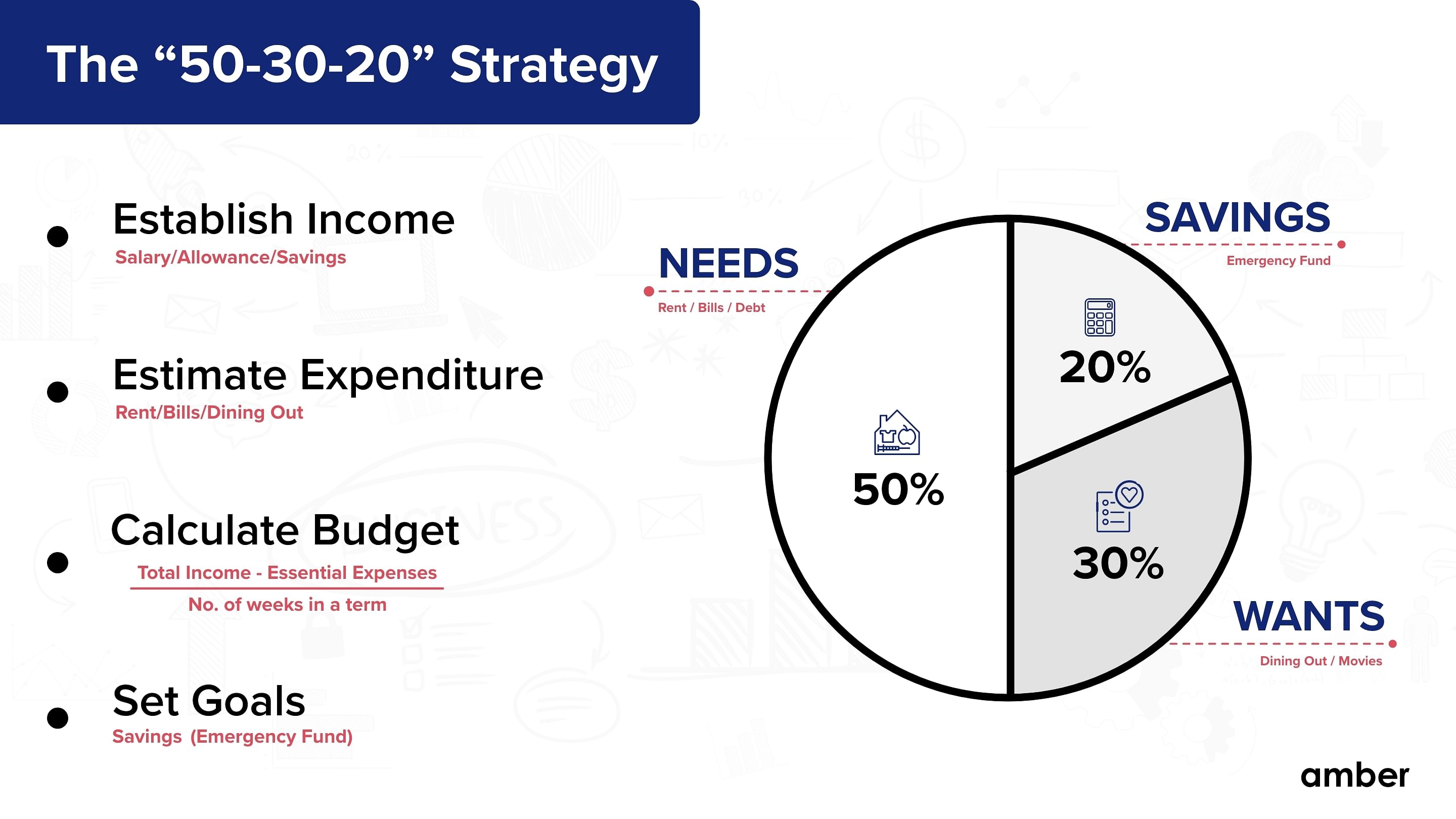

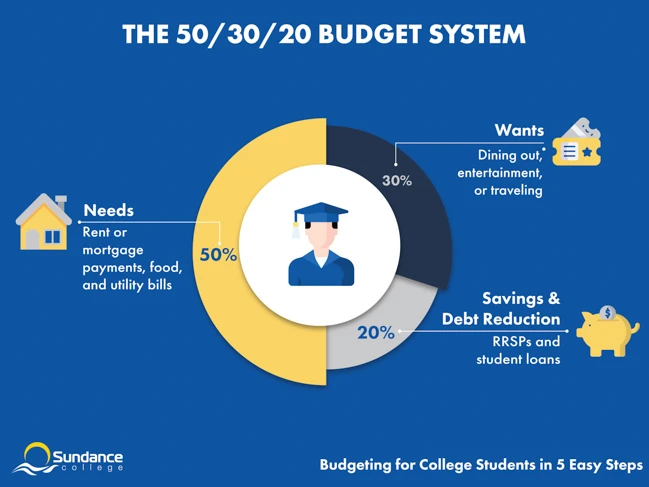

- 50/30/20 Rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

- Zero-Based Budgeting: Allocate every dollar of your income to a specific category, so your total income minus total expenses equals zero.

- The Envelope System: Use cash for variable expenses, placing the allocated amount for each category (e.g., groceries, entertainment) in separate envelopes.

Steps to Create a Budget

- Calculate your total income: Add up all your income sources for a specific period (e.g., monthly).

- List your fixed expenses: Identify expenses that remain consistent each month.

- Estimate your variable expenses: Use past spending data to estimate these costs.

- Allocate your income: Use a budgeting method to distribute your income across expense categories and savings.

- Track your progress: Regularly compare your actual spending to your budgeted amounts and make adjustments as needed.

- Review and adjust: Your budget isn't set in stone. Review it monthly and make changes to reflect changes in your income or expenses.

Tips for Sticking to Your Budget

- Set realistic goals: Don't try to make drastic changes overnight.

- Prioritize your needs: Ensure essential expenses are covered before allocating money to wants.

- Find ways to save money: Look for student discounts, buy used textbooks, and cook meals at home.

- Avoid impulse purchases: Wait 24-48 hours before buying non-essential items.

- Use cash when possible: This can help you visualize your spending and avoid overspending.

- Find a budgeting buddy: Accountability can make it easier to stick to your budget.

- Reward yourself (occasionally): Budgeting doesn't mean deprivation. Allocate a small amount for guilt-free spending.

Budgeting for Specific Student Expenses

Tuition and Fees

Tuition is often the largest expense for students. Explore these options:

- Financial aid: Apply for scholarships, grants, and work-study programs.

- Payment plans: Many universities offer installment plans to spread out tuition costs.

- Tax benefits: The American Opportunity Tax Credit and the Lifetime Learning Credit can help offset education expenses.

Housing

Whether you live on-campus or off-campus, housing is a significant expense.

- On-campus housing: Factor in dorm costs, meal plans, and resident hall fees.

- Off-campus housing: Consider rent, utilities, internet, and transportation costs. Look for roommates to share expenses.

Food

Food costs can add up quickly.

- Meal plans: Evaluate if a meal plan is cost-effective for your eating habits.

- Grocery shopping: Create a meal plan, make a shopping list, and cook at home to save money.

- Student discounts: Many restaurants offer discounts to students.

Textbooks and Supplies

Textbooks can be a major expense each semester.

- Buy used textbooks: Purchase used books from online retailers or upperclassmen.

- Rent textbooks: Renting can be significantly cheaper than buying.

- Digital textbooks: Consider e-books, which are often less expensive.

- Library resources: Check if your library has the required textbooks.

- Share with classmates: If possible, share textbooks with friends.

Transportation

Transportation costs vary depending on your living situation and how you get around.

- Public transportation: Many cities offer student discounts on bus or train passes.

- Walking or biking: These are free and healthy ways to get around campus.

- Carpooling: Share rides with classmates to save on gas and parking.

- Student parking permits: If you bring a car, factor in the cost of parking permits.

Health Insurance

Health insurance is essential for all students.

- Student health plans: Many universities offer health insurance plans for students.

- Parent's insurance: If you're under 26, you may be able to stay on your parents' plan.

- Medicaid: If you meet certain income requirements, you may qualify for Medicaid.

Long-Term Financial Planning

Building an Emergency Fund

An emergency fund can help you cover unexpected expenses, such as medical bills or car repairs. Aim to save 3-6 months' worth of living expenses. Even small contributions can add up over time.

Saving for the Future

Start saving early for long-term goals like graduation trips, or even retirement. Consider these options:

- Savings accounts: Look for accounts with competitive interest rates.

- Roth IRA: A retirement account that allows your investments to grow tax-free.

- Investing: Explore low-risk investments like index funds or ETFs (Exchange-Traded Funds).